This was published in HFM-CTA Intelligence magazine in February 2020. Link here.

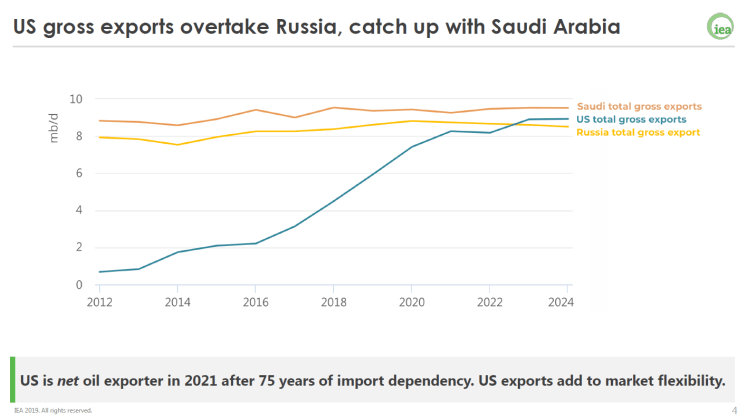

As the decade draws to a close, we note a quiet but staggering milestone – the world consumed more than 100 million barrels of oil per day. In addition, the shale oil & gas revolution in North America has upended the established geopolitical order in which the US is a price taker and is compelled to intervene in far-flung places out of self-interest. In 2016 the Saudis tried to flood the market but failed to decapitate shale production. Since then OPEC has been playing defense by cutting production and biding its time in waiting out the storm. Beginning in 2020 that strategy may finally bear fruit.

Figure 1 – IEA: US, Russia, Saudi Arabia Oil Export 2012-24

In 2019 a few significant events developed or continued to play out that shape our view of 2020 and beyond. Here are ten observations.

- The shale revolution appears to be running up against a wall. From longer laterals to higher proppant intensity to downspacing, production growth had been phenomenal thanks to relentless innovation. Now that some industry experiments, most notably by Concho Resources, had revealed the limits of downspacing due to parent-child well interference or cannibalization, the perception is that the tricks are running out.

- Enhanced oil recovery (EOR) in shale formations using associated natural gas, is another experiment that is garnering attention and effort, starting in Eagleford Shale. Especially when natural gas is considered a waste product by many Permian Basin oil producers due to the lack of takeaway pipelines. But the added recovery is incremental and likely not enough to move the needle.

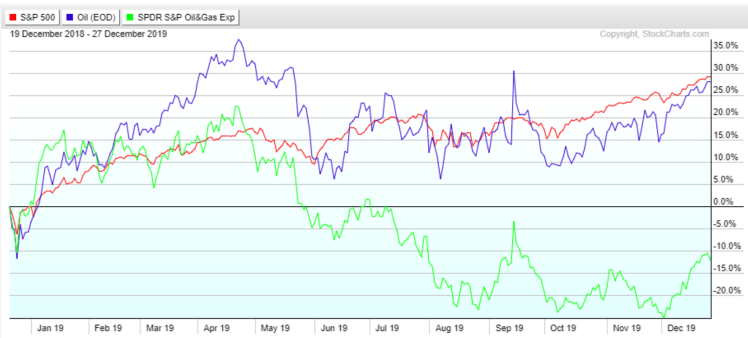

- Public investors have started to perceive the end of an era when production grew by leaps and bounds. Beginning in 2019 investors have been bailing on oil & gas sector en masse. Since the sudden crash in 4Q18 crude oil has massively outperformed oil & gas stocks (+20% vs -20%). And in the past ten years, energy’s share of the broad S&P Index has steadily dropped from 13% to 5%, reflecting very negative sentiment.

Figure 2 – 1-year performance: S&P 500, West Texas Intermediate Crude, S&P Oil & Gas Exploration Production ETF

- Demand expectations have been hampered by threats from trade war and the likely end of the longest economic expansion in history. OPEC, IEA, and EIA forecasts have all indicated surplus ranging from 200,000 to 800,000 bbl/d.

- Investors who are still invested in oil & gas have been demanding capital discipline from companies. Free cash flow, not production growth, is king. Companies found themselves shut out of public equity and debt markets. Valuations have come down. Bank credits are harder to come by. Private companies are looking to hold assets for longer, due to the lack of interest from buyers and less exit options from sellers.

- Since scale allows companies to lower G&A, optimize production footprint, leverage service providers, and grow within cash flow, it makes sense for industry consolidation. Companies with strong balance sheets and short of long term drilling inventory in prime basins will be especially keen, for example Occidental gobbling up Anadarko. M&A activity may pick up while asset-level A&D continues to languish because markets are currently not giving much credit to undeveloped reserves or non-cash generating assets.

- Climate change activism has picked up steam globally and negative sentiment toward fossil fuel should continue intensifying for the foreseeable future. Peak oil demand has been touted a lot in 2019. Long term, electrification will eat into transportation demand; battery technology will boost renewables share in power generation. The hardest area to replace oil & gas is materials made with petroleum products.

- That leads to the rationale and urgency of Saudi Aramco’s ~$2-trillion IPO, the biggest the world has ever seen. Their explicit goal is to grab the cash while they can to diversify an overly oil-dependent economy, starting with investments in petrochemical industry.

- On the supply side, geopolitical events that historically caused spikes were received with equanimity. Effects from the Strait of Hormuz tension (20% of world oil traffic), collapse of Venezuelan production and export, and the Saudi oil facility attack (5% of world production) were almost muted. Even the Iranian attack on America’s Iraqi bases in January was met with relative calm. With the startup of major export pipelines from the Permian Basin to the Gulf Coast, the market will also become more balanced and WTI-Brent spread should tighten in 2020.

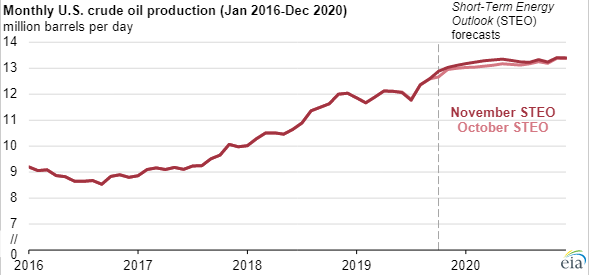

- American shale producers have found too much oil for consumers to keep up in recent years. However, due to capex reduction, production growth from the U.S. is expected to slow to under 1 million bbl/d in 2020 and toward zero in 2021, from its breakneck pace in 2018/19. But the “shortfall” from the Americans can easily be made up by OPEC countries who retain much spare capacity, despite their 2017-2020 production cut agreement. OPEC’s (reluctant) strategy of waiting out the shale gale was ineffective in the last few years but is beginning to bear out.

Figure 3 – EIA: US Crude Oil Production 2016-20

Since writing about the structural decline in oil’s volatility in 2017, our central thesis of this balance of forces between OPEC’s massive swing production and American shale’s fast response time has borne out, resulting in the compressed commodity cycle and relatively tight price range. To the extent that an estimated 1 million bbl/d of new oil from Norway and Brazil coming onstream next year, it is more or less a one-time event. Would anything be fundamentally different in 2020? Not unless you count the slight shift of power back into the hands of OPEC. With a fair balance between sheiks vs shale, it is hard to see prices make a big move either way. However, the nagging threat of a recession could mean there is an asymmetric setup for a downside move.

Jeff Lee, CTA

Kronos Management, LLC

January 9, 2020

Opinions expressed in this document are for general informational purposes only and are not to be construed as an offer, recommendation, solicitation, or investment advice. Kronos Management makes no representation or warranty relating to any information herein, which is derived from independent sources. Trading commodities bears substantial risk of loss, and is not suitable for all investors. Please consider your financial condition prior to investing with Kronos. For further details regarding the risk of trading with Kronos, refer to the Disclosure Document.

You must be logged in to post a comment.