This article was also published in Alpha-Week on October 8, 2018.

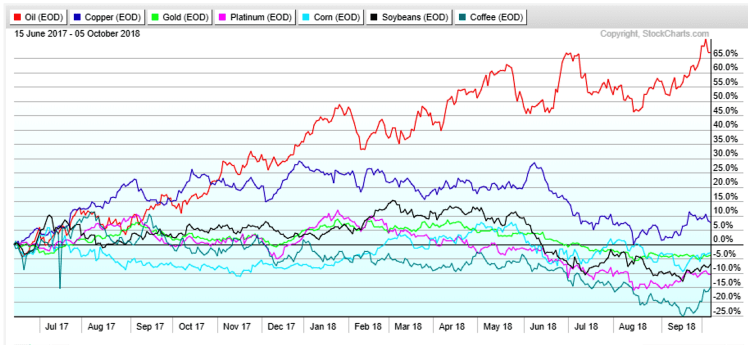

Since hitting bottom at $42 last summer, West Texas Intermediate (WTI) oil has staged an impressive comeback to trade in the $60-$76 band. Even more impressive is that it is pulling away from almost all other major commodities. In this issue we briefly examine the moving parts and address the current state of affairs, mostly to answer the question: how sustainable is this uptrend?

Figure 1 – Oil vs the Rest

First things first. In commodity markets, one always has to remember the second-order effect – all the headlines of conflicts, outages, and natural disasters matter, but only to the extent of their effects on the underlying trends in supply and demand. Commodities have end users, so when the fundamentals exert themselves, especially on the margin, minor events can create shocks. When sentiment runs ahead of fundamentals, even minor positive news are exaggerated; when sentiment sours, every minor bad news brings intense selling pressure. In light of the remarkably stable demand and the upcoming Iran sanctions, we argue that oil is poised for further upside, albeit limited, in the near term, but face significant headwinds in later half of 2019. Consider the following:

- Supply/demand is widely considered to be tight and remain so until late 2019. American refineries have been running above 95% utilization but are barely keeping up with demand. Global fiscal and monetary stimulus remain intact to goose economic growth, though on increasingly shaky grounds.

- The general sentiment for oil among analysts and investors are still extremely bullish. Managed money long/short gap has been very wide all year and strong pricing backwardation shows no signs of reversing.

- Seasonality is a headwind as we head into winter low demand season but crude inventory levels are trending decidedly lower and are now below 5-year average.

- Saudis are content with the current price level (Brent $70-$85) as it stabilizes their budget. Although they have ramped up production since March to counter Venezuelan and Iranian decline, President Trump is expected to escalate the rhetoric for OPEC to “do something” about oil (read: gasoline) ahead of the midterm election. Symbolic gestures in the form of a mild production boost is likely.

- America’s European and Asian allies are expected to comply with the November Iran sanctions. Most have already drastically cut back Iranian imports. One of Iran’s biggest customers India was recently caught receiving an off-grid Iranian tanker but it should be an anomaly. China on the other hand, can be expected to circumvent the U.S., especially when it is cutting American oil imports in light of the trade war.

- Saudi Arabia is about the only country with any meaningful spare capacity. This is widely believed to have dwindled down to around 1.5 to 2 million bopd, which at 1%-2% of overall global demand is limiting their ability to manage prices and is create a potentially disproportionate upside shock.

- Despite declining capital efficiency, U.S. shale oil producers are still operating comfortably above their breakeven prices ($30s to $40s) and are already hedged out for the next few years. They are, however, struggling mightily to increase production, fighting constraints on takeaway capacity, water disposal, sand, trucks, and inflation. Production is at record high but is expected to flatten out in 2019. Rig counts are revealing: they are declining in the most prolific Permian Basin but increasing in other basins, though it will take a few months to materialize into production.

- The latest EIA survey showed that the gap between drilled wells and drilled but uncompleted (DUC) wells in the Permian Basin is rapidly widening, signaling producers’ desire to time production to new pipelines coming online at the end of 2019 to avoid the wide Midland-Gulf Coast discount.

The last two points are not trivial. While OPEC provides the big chunk of the world’s oil and the Saudis, with their large spare capacity, manage the production swing, Permian Basin, by its sheer size and velocity, has become a critical marginal producer that carries an outsize influence. We are not sure how much excess DUC inventory will be built when all is said and done, but we do believe that given time it can develop into a significant drag on prices. When pipelines are completed or if prices break and producers rush to complete the wells and turn on the tap this could exacerbate any downward movements.

Give that economic growth, and by extension, equity markets and risk appetite, are stable for now, there are few catalysts to dislodge oil from the current uptrend. The few bearish factors are mild and non-structural. In fact, geopolitical tensions have not been this subdued for a while, setting up an asymmetrical situation for an upside move for the next few quarters.

Jeff Lee

Kronos Management, LLC

September 21, 2018

Opinions expressed in this document are for general informational purposes only and are not to be construed as an offer, recommendation, solicitation, or investment advice. Kronos Management makes no representation or warranty relating to any information herein, which is derived from independent sources. Trading commodities bears substantial risk of loss, and is not suitable for all investors. Please consider your financial condition prior to investing with Kronos. For further details regarding the risk of trading with Kronos, refer to the Disclosure Document.

You must be logged in to post a comment.