This piece appeared in HFM-CTA Intelligence August issue (pdf here). HFM link here.

Equity markets in January feels like a long time ago when new highs were posted day after day. Then things got interesting in February, when the volatility kraken was suddenly awoken by the prospect of 3% 10Y yield, as if no one saw it coming. What followed was a flurry of seemingly earth-shaking events – new Fed chair, North Korea, global trade war fear, record U.S. Treasury auction, White House’s appointment of hardliners, Facebook scandal, Syria escalation, among others. Since then many of these events seemed to have softened or reversed. Even a recent escalation of trade war with China has ceased to ruffle any feathers. Volatility has come back down to earth.

Investors have long known that things don’t matter until they do. 2017 saw a lot of disturbing events but the market shrugged them off. Headlines are misleading if no context is given, and even more so if the human feedback loop is disregarded. George Soros famously captures these dynamics in his reflexivity concept. Fundamental factors affect sentiment and prices on the margin, analogous to fracture mechanics: initiated cracks can continue to exist in a material until an incremental load pushes it over the edge and the energy releases itself in the form of propagation, and the system collapses. The crack only stops running when enough energy has been released to arrest the crack. One can also draw an analogy to the assassination of Archduke Ferdinand that precipitated World War I. Without the enormous build-up of tension among the European powers this act would not have triggered the chain reaction of war declarations. The pent-up energy was released when the parties subsequently exhausted themselves.

Figure 1: Fracture Mechanics: Stress-Strain Relationship

The way we see it, the February-May correction served to release some nervous energy in market participants. All the risk build-up in the last couple of years did not appear to break the sentiment but they did end up somewhere in the system, in the form of increased fragility. We don’t know where the straw is going to come from to break the camel’s back but we believe this recent correction has brought the next downturn closer.

Markets are clearly in a state of flux. We echo the CME Group’s analysis calling this period a phase transition akin to a pot of boiling water with great turbulence at the top and calm beneath the surface. Multiple price peaks and valleys had been created in a short period of time, but this is about more than price fluctuations. We see the beginning of macro themes moving markets, shifting correlations, central bank policy divergence, and a late-cycle commodity boom.

Rising Inflation/Yield

The stock market is likely in a late-stage rally. Tax cuts without reforms represent a major multi-year fiscal stimulus that raises inflation. The spending gap will need to be financed by more treasury sale, increasing future debt servicing costs at a time when the Fed is raising rates and unwinding asset purchases. Granted, the fiscal deterioration is a future event, and now that the rate hikes and Fed unwinding have been baked in the cake, a gradual rise of inflation and yield should not shock anybody. Treasury Secretary Mnuchin expressed confidence that there are enough buyers of U.S. treasury around, and since there is a general shortage of safe assets these days he is probably right. European economic weakness and political headwinds are reinforcing policy divergence between the Fed and ECB, boosting the dollar and suppressing yield, but U.S. twin deficit should exert pressure longer term. It is a very complex development that requires constant monitoring.

Trump Unbound

President Trump’s 1950’s version of American prosperity and world pecking order, his worship of money and business, his need to feed his ego and popularity, his transactional view on relationships, and his underdog mentality are very telling. From his fondness of resources and heavy industries, handling of racial issues, hostility to regulations/environment in favor of businesses, tax cuts for the wealthy, shrinking from Chinese trade pushback, withdrawing from Iran nuclear deal, to his “TV-ready” combative approach, his moves can be uncertain but amusingly predictable.

Unfortunately, in conducting American policies, the Trump administration constantly upsets the applecart and creates risky binary events with unnecessary uncertainty. As we approach the end of the bull market this is likely going to produce more choppiness than usual.

Rising Geopolitical Tensions

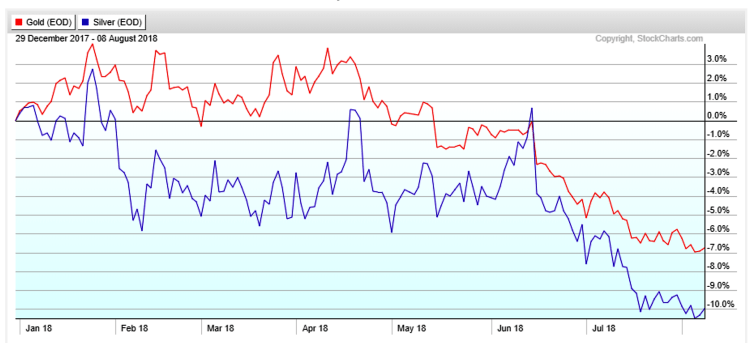

The dismantling of the Washington Consensus and America’s withdrawal from the world, particularly the Middle East, creates a power vacuum and unstable new alliances that have lasting implications. America is signaling a return to the free-for-all world order where the small fish survive at the mercy of great powers. China and Russia will seize on this to impose their world order while small countries scrambling to pick a side. The second order effect of this dynamic is not immediately obvious but the system is building up stress that should add risk premium to all asset classes over the medium term. As a matter of fact, shifting correlations are reflecting this: oil followed supply/demand last year before tracking the stock market in January, then geopolitics took charge since March. There has also been a consistent backwardation in crude futures contracts. Gold was vulnerable to interest rates and the dollar for a long time until risk-off sentiment kicked in in February. One place where this shows up is the persistent gold/silver price spread.

Figure 2: Gold-Silver Relative Performance (2018)

Rising Protectionism and Populism

Trade wars are hugely influential on macro environment. Reduced international cooperation and rising domestic political pressure may affect global growth, currency moves, and political outcomes. Cases in point: Mexico election, American pork and soybean exports. While it remains to be seen how much existing trade flows will be disrupted, the current American administration’s mercantilism attitude is on clear display. There are no sacred cows and there are nearly no special relationships or strategic partnerships when it comes to “paying” America. Countries can buy good graces by importing more American goods or simply giving the president a good headline, every so often. The Saudis scored points by buying more American weaponry; the South Koreans were punished on a trade agreement in the middle of a North Korea nuclear crisis talk. NAFTA talks were linked to the Mexican wall while the popularity of the populist Mexican presidential candidate is surging.

Protectionism tends to cause concentrated gain (producers) and large distributed pain (users), which only makes short-term political sense. The worst part is not only the haphazard implementation of trade tactics, or that cold economic logic takes a backseat to manufactured rhetoric that fits the America First narrative. It is the non-cooperation among countries and the disintegration (without replacement) of the World Trade Organization that could lead to disastrous economic outcome for all.

Volatility Will Return

These phenomena do not exert themselves in isolation. In a dynamic, non-linear system, outputs often become inputs; effects on the margin are disproportionately large.

History (and future) is path dependent. After decades of American hegemony, the institutions formed after World War II have created unprecedented wealth but have also shown signs of age. The macro themes discussed above are largely a reflection of the inequality, globalization, financial excesses, and the complacency of politicians. The process of formulating solutions to these problems is messy and the turbulence we are witnessing is not going to fade quickly. The relentless decline of VIX index reflects the need for hedging from the reluctant investors who are buying into the increasingly narrower and shakier U.S. stock markets. In fact, the stage is set for the volatility kraken to be awakened in the near future.

Disclaimer:

Opinions expressed in this document are for general informational purposes only and are not to be construed as an offer, recommendation, solicitation, or investment advice. Kronos Management makes no representation or warranty relating to any information herein, which is derived from independent sources. Trading commodities bears substantial risk of loss, and is not suitable for all investors. Please consider your financial condition prior to investing with Kronos. For further details regarding the risk of trading with Kronos, refer to the Disclosure Document.

You must be logged in to post a comment.