Over the past few months on Wall Street, firm after firm has issued analyses that point to the new dawn of commodities in 2018 and beyond. At the risk of sounding cliché, we agree. In fact, since May of 2017 we have written about the changing macro winds. Now that stock market volatility has reared its ugly head, Barron’s has a nice piece on diversifying into commodities for the average investors. See article here…

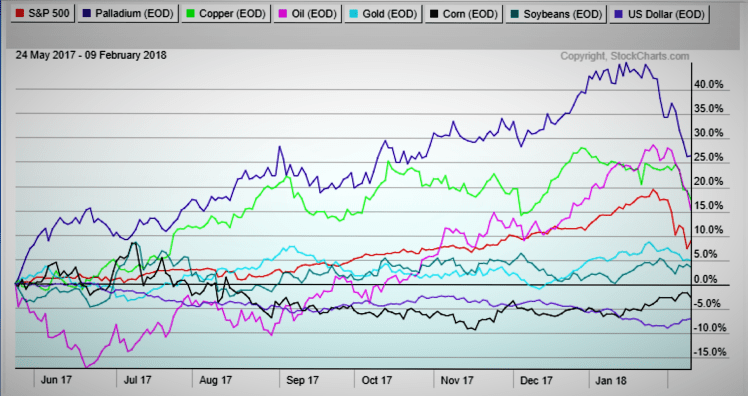

This wave started slowly last summer with base metals, meats, energy, precious metals, and now even grains look healthy. Of course not all commodities are created equal. Base metals and meats are likely to continue to do well based on economic growth. The energy complex looks a bit stretched at the moment but should keep its gain. Precious metals will experience some headwinds due to rate hike expectations but inflationary pressure and safe haven demand might provide a floor. Grains are showing signs of life thanks to strong demand growth and tightening market conditions.

Consensus view on the US dollar is continued weakness. In fact, the strength of euro and the aggressiveness of the dollar’s downward move recently have surprised many. Inflation and rate hike expectations hammered the bond market in January then the stock market in February. There has been some recalibration of correlations among asset classes.

Dow’s near 2,000+ point drop in a week and near 3,000-point travel have caused a lot of angst and awakened the volatility kraken. Market participants seem to have begun the transition to risk-off mode. However, late stage rallies are usually choppy and messy. It will take a much larger shock for people to run to safe assets en masse. When that happens, which is a long ways off, precious metals and bonds should be in vogue again. In the boiling frog analogy, the frog has just received a jolt from a hot spot in the warming pot – it’s not ready to jump out just yet.

On another note, shutdown politics has played out twice in a month. Alas, that old fashion kick-the-can-down-the-road still reigns. The latest compromise calls for more military AND domestic spending without a trace of reform of the big three – defense, Social Security, and Medicare, at a time of record debt level and rising interest rates. It is cliché to blame politicians, but it is hard not to – this is not a good time to put another new car on the family credit card. What could go wrong? China has already signaled a move away from US Treasury purchase and the post WWII international order is in a terminal decline, along with American hegemony. Our system is robust and resilient but it can only take so much abuse. In engineering, once a crack is initiated it can stay dormant while stress builds. This can last a long time until a trigger causes it to propagate. This propagation phase is catastrophic, and it is every engineer’s nightmare. We think of the current state of economy/ debt/ spending/ credit the same way. Without another economic renewal and no political solution in sight, it is hard to foresee a happy ending.

Overall, we agree with the consensus that commodities’ time has arrived. Long term structural dollar weakness, tightening market conditions, strong demand are supportive of prices. Our indicators of improving fundamentals, good technical picture, and positive sentiment are all present. We are confident that our macro thematic trading will benefit from this development. In fact, EMMA program’s correlation to S&P 500 just hit 0 at the end of January.

February 9, 2018

You must be logged in to post a comment.