Recent rout in oil has been hogging the headlines. Our prognosis on oil’s downtrend in May has played out with conviction so far in June. Now we turn to the outlook of oil’s poor cousin, natural gas.

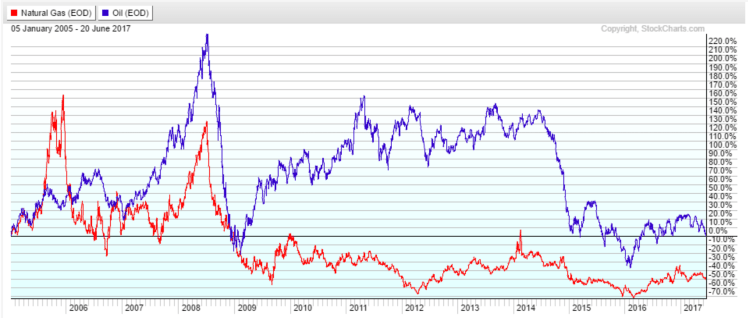

American gas was hit by the shale revolution a few years earlier than oil, and its price depression due to the unleashing of prodigious amount of resources has foreshadowed that of oil’s. The fungibility of oil however, has somewhat shielded it by allowing it to be traded around the globe and spreads arbitraged away. The fortune of the two commodities as highlighted in this chart dating back to the start of the shale revolution is telling.

Structural Changes Are Painfully Slow

Support for the gas market is emerging but slowly. Since the big crash in 2009, structural changes in the domestic power markets, petrochemical feedstock, LNG export, Mexican energy reform, and to some extent, gas-powered vehicles and small scale LNG/CNG technologies have emerged to absorb the excess supply. Granted, the gas market may never achieve the efficiency of liquid and solid fuels markets due to the complexity of processing and difficulty of transportation. And prices have also been doomed by the overhang of the monstrous resources in the still-untapped shale rocks. For these reasons gas has been undergoing a more painful adjustment and a recovery that seems to never end.

Summer of Hope

Nevertheless, the current state of affairs for gas is fairly healthy. Despite the price slump in May in response to the lackluster demand in the shoulder season, most major weather forecasts are still calling for above average summer temperatures for the Northeast and the South where the cooling demand is. In fact, Cooling Degree Days (CDD) have been trending steeper than 5-yr average.

Inventory level is slightly above normal and most analysts appear to believe that it is going to enter the 2017/18 heating season below trend even with a normal summer. LNG export, Mexican export, and industrial demands are all picking up and are expected to continue the momentum. Coal-to-gas switching at power plants has been trending up since 2005 and has seen higher highs in most years. Although gas prices are higher than last summer, coal prices have also recovered some, enabling gas to remain competitive. In addition, the heat rate (efficiency) of gas-fired power plants have improved meaningfully in recent years while coal plants stayed the same. This means that less gas is required to generate a given MWh but it is more than offset by the major impetus to displacing coal. Since power is the biggest demand center for gas in the summer, we expect weather fluctuations to play a very critical role.

Speaking of weather, predictions of hurricane season’s early arrival and higher intensity this year appear to have a muted effect. The Gulf of Mexico’s production is not as impactful as before, and the potential disruption of LNG export terminals in the Gulf Coast may even be a major offsetting factor one day. That would be an interesting turn of events.

On the other hand, since peaking in 2015, gas production has been flat this year despite the doubling of gas rig count from last summer thanks to natural decline from wells drilled in the previous cycle. Signs of renewed production growth in Haynesville and Marcellus shales threaten to derail the recovery but until major takeaway pipelines from the Northeast are completed on schedule over the next three years there is no imminent danger of a gush. The stagnant rig count in Marcellus can attest to that.

Putting It Together

Natural gas as a commodity is notoriously volatile but the convergence of supply and demand does not necessarily promise calm. The quirky seasonality and storage constraints have always been major considerations but the relative shortage of storage and the increasing market share of gas in power generation mix are raising the sensitivity of prices to weather and incremental production. Linear thinking does not apply when changes on the margin have a disproportionate effect – witness what the haggling of ½% of world oil production does to prices. As more coal power plants are retired and replaced by gas fleets, we envision the total demand curves to exhibit a more pronounced double-peak pattern in the coming years.

The recent plunge in managed money net length since May, when viewed in the context of the short term and medium term factors, appears to be setting natural gas up for a promising summer.

Kronos Management, LLC

May 30, 2017

Opinions expressed in this document are for general informational purposes only and are not to be construed as an offer, recommendation, solicitation, or investment advice. Kronos Management makes no representation or warranty relating to any information herein, which is derived from independent sources. Trading commodities bears substantial risk of loss, and is not suitable for all investors. Please consider your financial condition prior to investing with Kronos. For further details regarding the risk of trading with Kronos, refer to the Disclosure Document.

You must be logged in to post a comment.